All analyses in this article are based on the ministry’s audited financial reports.

Reference: North Hatley’s 2024 audited financial reports

Some may say that I am insisting on this point—I readily admit it. However, since this issue has already led to a formal notice being sent to a citizen, I believe it is legitimate to continue discussing the issue of municipal debt. My goal is simply to better understand the explanations provided by the municipality and to compare them with those put forward by Mr. Reed.

It should be noted that the intention is not to blame anyone, but rather to understand the actual situation of North Hatley’s municipal debt by asking questions.

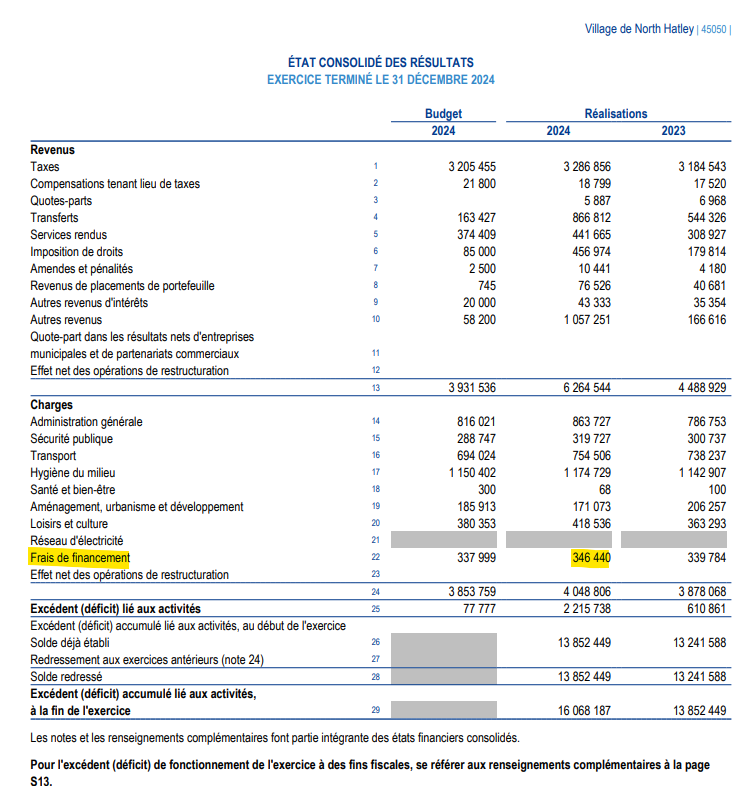

Or, en consultant les états financiers audités de 2024 disponibles sur le site du ministère depuis quelques jours, j’ai constaté que les frais de financement s’élèvent à 346 440 $. Bien que je ne sois ni fiscaliste ni comptable, une simple règle de trois permettrait déjà d’estimer le montant total de la dette municipale.

However, when consulting the audited financial statements for 2024, which have been available on the ministry’s website for several days, I noticed that financing costs amount to $346,440. Although I am neither a tax specialist nor an accountant, a simple rule of three would already allow me to estimate the total amount of municipal debt.

Note: Rates vary from one loan to another. The idea is to provide an overview.

Let’s calculate the debt based on financing costs.

I don’t know the exact interest rate on the municipality’s loans. In the reports, the city’s borrowing rates range from 1.5% to 5.2%. The Bank of Canada’s key interest rate is 2.5% today. Let’s take the key rate + 1% to be reasonable. If you disagree, leave a comment and I will adjust it.

Calculate the debt with a financing rate of 3.5%

Financing costs 2024

346 440$

Interest rate (prime rate + 1%)

3,5%

Debt

Unknown

Equation for calculating financing costs

Debt X 3,5% =346 440$

Rule of three for estimating related debt

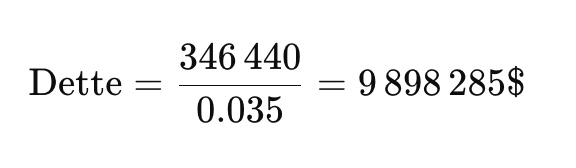

346 440$ / 3,5% = 9 898 285$

It should be noted that this amount is close to the amount put forward by Mr. Reed.

The interest rate is unknown, so let’s calculate two scenarios.

Be careful, if I take a lower interest rate, it means that my debt is even higher. With a 5% interest rate, this indicates that my debt would be 6.928 million. Perhaps the interest rate on the debt is even higher, which would indicate a lower debt. So let’s take 5%.

Calculate the debt with a financing rate of 5%.

Financing costs 2024

346 440$

Interest rate (estimation)

5%

Debt

Unknown

Equation for calculating financing costs

Debt X 5% =346 440$

Rule of three for estimating related debt

346 440$ / 5% = 6 928 800$

It should be noted that this amount is close to the figure put forward by the municipality in its newsletter dated October 1.

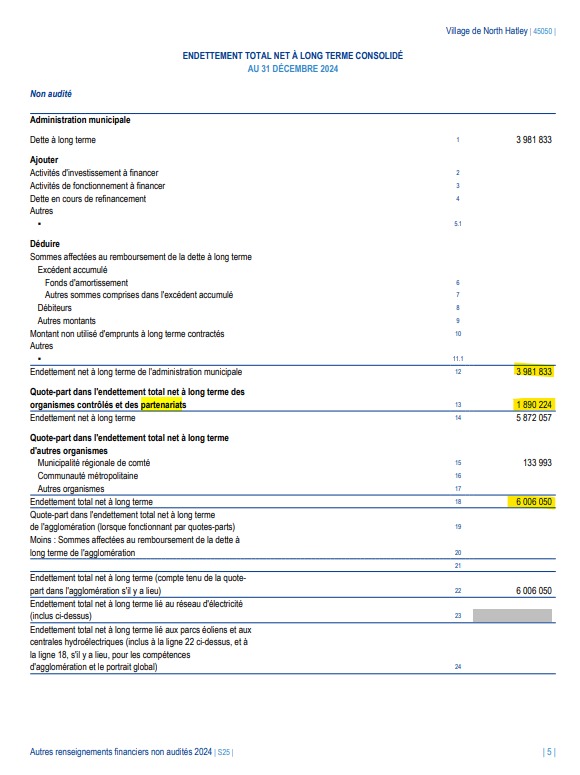

Debt in the 2024 financial report

In my opinion, these figures represent the reality of municipal debt. We have the municipality’s figures of $3,981,833 in long-term debt and $1,890,224 in contributions to organizations. This gives a net long-term debt of $6,006,050.

Based on the amount of debt, let’s calculate the average interest rate applied.

Financing costs 2024

346 440$

Interest rate

Unknown

Debt

6 006 050$

Equation for calculating financing costs

6 006 050$ X Unknown = 346 440$

Rule of three for finding the average interest rate

346 440$ / 6 006 050$ = 5,7% average interest costs.

It should be noted that this amount is close to the figure put forward by the Municipality in its newsletter dated October 1.

To this figure must be added other obligations.

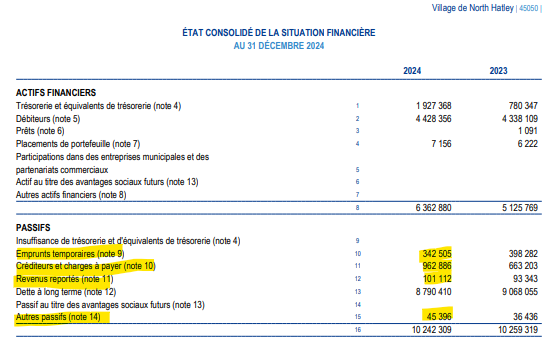

Temporary loan = $342,505

Accounts payable and accrued liabilities = $962,886

Deferred revenue = $101,112

Other liabilities = $45,396

Subtotal other = $1,451,889

Total net long-term debt = $6,006,050

Subtotal other obligations = $1,451,889

TOTAL DEBT as of December 31, 2024 = $7,457,949

Who is telling the truth, the municipality or Mr. Reed? That’s not important; what matters is asking questions to ensure that our financial reports reflect reality.

The composition of interest on financing costs

Please note that the $346,440 in “financing costs” is not solely interest on long-term debt; it may include interest on temporary borrowings, consolidated share of interest, and accounting fees related to debt. Therefore, a single rate cannot be deducted without taking this composition into account.

In conclusion, the important thing is to ask questions.

What I am questioning is not so much the results presented as the municipal administration’s method. I am well aware that managing a municipality is complex and demanding. However, questioning is not criticizing for the sake of criticizing—it is seeking to understand.

Asking questions is essential when it comes to public finances. It helps clarify information, avoid misunderstandings, and bring the municipality’s explanations closer to those raised by Mr. Reed. This is how we build public trust: through transparency and consistency.

Encore une fois, j’espère que cela vous aura permis d’en apprendre un peu plus. Pour ma part, l’exercice a été très constructif !

It should also be remembered that the purpose of a meeting to present financial statements is to provide citizens with a complete, balanced, and accurate picture of the financial situation. However, the PowerPoint presentation on September 16 only highlighted a selection of positive information, leaving out several essential aspects that should have been explained.

A simple mea culpa from the municipality would have been enough to acknowledge this lack of balance and restore confidence. To err is human. To persist without acknowledging the error is less so.

For my part, if I have the honor of being elected, I will consider it healthy and necessary for citizens to ask questions about public finances. An informed and engaged population is not an obstacle for a municipal administration—it is its best ally for transparent and responsible governance.

Once again, I hope this has helped you learn a little more. For my part, the exercise has been very constructive!