This article aims first to define the decommissioning of fixed assets (OMHS) in order to support other texts on related issues. The objective is to clarify what these expenses cover and their impact on the municipality’s future debt.

As the debt was highlighted in the September 6 municipal newsletter, mentioned in the formal notice sent to Mr. Reed, and then explained in the October 1 newsletter, I looked into the matter further and spoke with colleagues to ensure that the financial information accurately reflects the situation. These discussions highlight a significant financial risk related to OMHS, which has not been mentioned to date and, to my understanding, is excluded from the 2023 and 2024 financial reports.

Obligations related to the decommissioning of fixed assets (OMHS)

Asset retirement obligations (ARO) correspond to the mandatory costs that the municipality will eventually have to pay to close, dismantle, or restore certain public facilities when they reach the end of their useful life.

This is a legal and environmental obligation. According to accounting standards, these costs must be planned for and recorded in financial statements since April 2022.

Exemples concrets pour une municipalité comme North Hatley

| Municipal immobilization | What may happen one day | Potential OMHS costs |

| Sewage pumping station | End of life or replacement | Dismantling + transport of materials + environment |

| Sewer system | Aging or reconstruction | Soil removal and remediation |

| Municipal dock or waterfront structures | Instability or non-compliance | Demolition + restoration of the riverbank |

| Municipal fuel tanks | Environmental risk | Soil decontamination |

| Municipal partnerships (e.g., waste management authority) | Closure of a landfill site | Post-closure management for 20 years |

| Municipal buildings | Reconstruction or demolition | Safe demolition + material recycling |

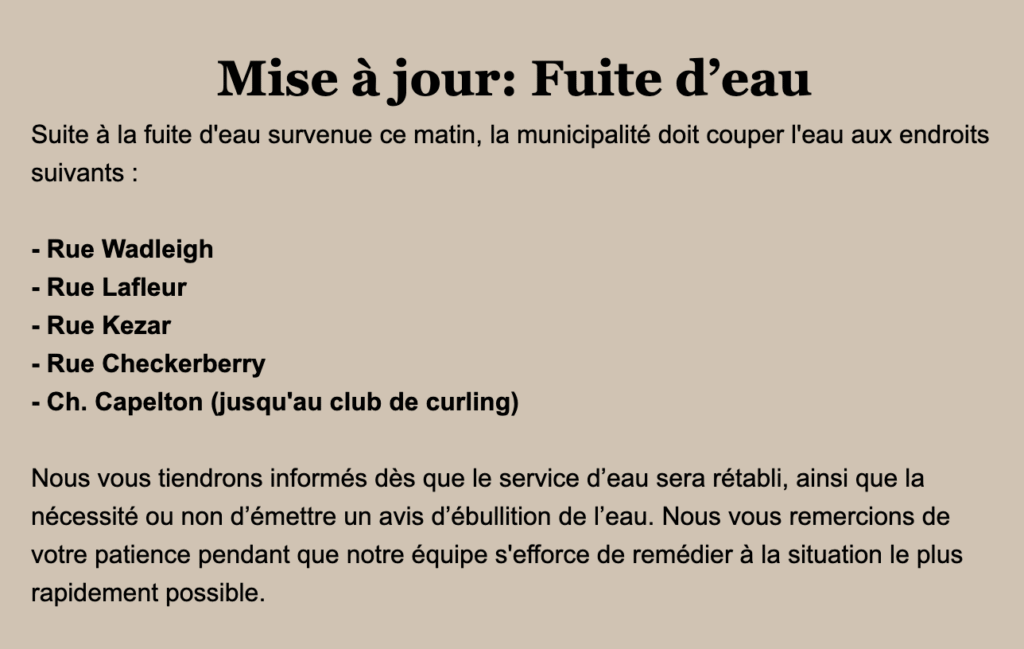

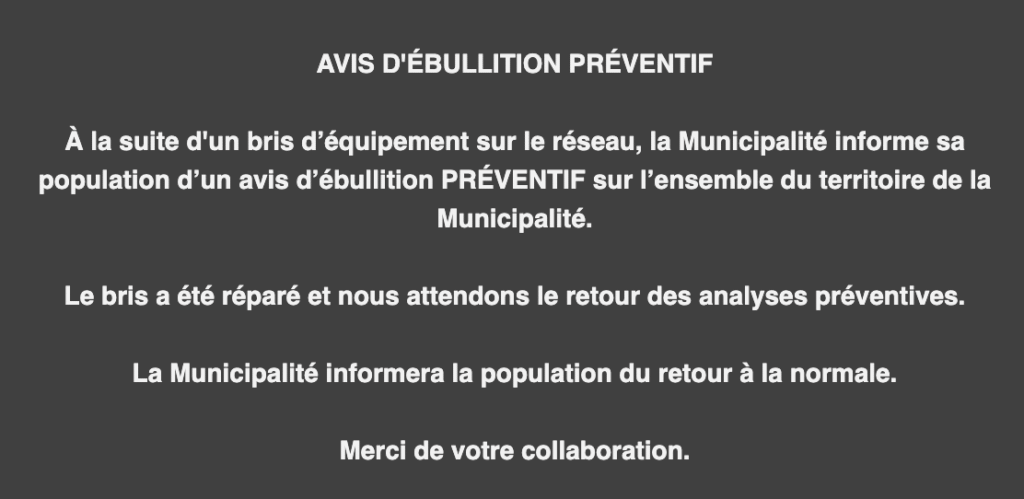

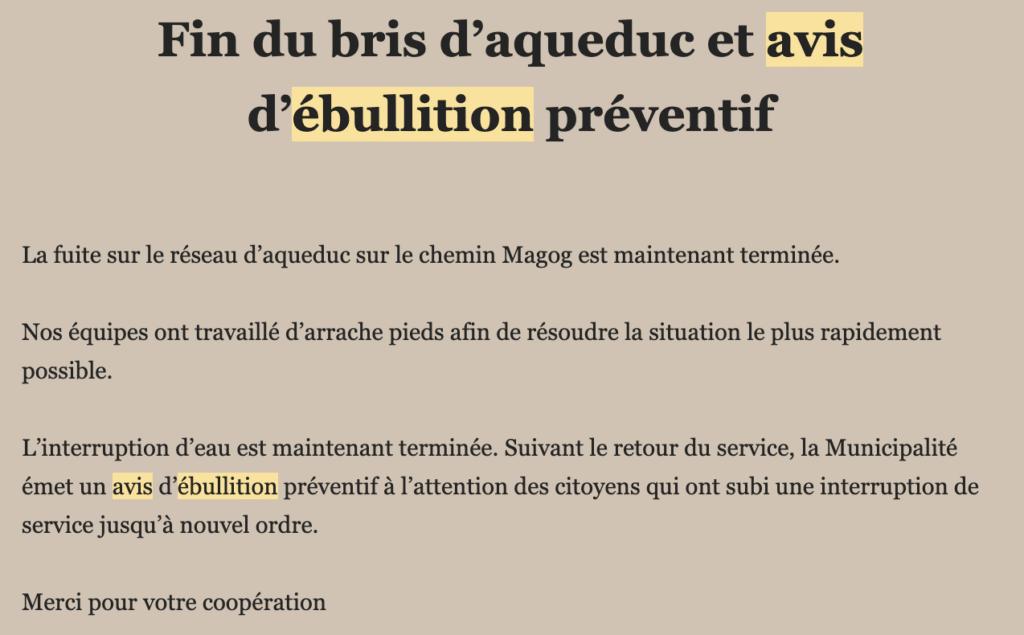

Water main breaks seem to be occurring more frequently, leading to numerous boil water advisories.

Does our water system require major repairs? If so, is this reflected in our budgets? The law requires that this be reflected in the municipality’s financial reports.

Remember the floods at the end of May 2025

Reference : https://www.northhatley.info/en/2025/05/23/are-we-prepared-for-a-civil-protection-emergency-in-north-hatley/

Why is this important for citizens?

Because these are unavoidable costs… and do not appear to be budgeted for in 2023 and 2024 by the municipality, according to the auditor’s report, which issues a qualified opinion. In fact, the auditor issued its financial statements with a qualified opinion stating that the financial information related to OMHS was not provided by the municipality. This means that future financial commitments are not visible in the current financial statements.

Note from the financial auditors in the audited report 2024

Basis for Qualified Opinion As at December 31, 2024 and 2023, with the exception of one of the partnerships that recognized a liability for a fixed asset decommissioning obligation related to its landfill site closure and post-closure activities, the municipality did not measure or recognize any liabilities for asset retirement obligations, did not provide the required disclosures on asset retirement obligations, and did not determine the adjustments to other items in the financial statements, which is a departure from Canadian Public Sector Accounting Standards. The impact of this departure on the financial statements for the years ended December 31, 2024, and 2023 could not be quantified. This situation therefore leads us to express a qualified opinion on the financial statements for the year ended December 31, 2024, as we did for the financial statements for the year ended December 31, 2023.

Référence : https://www.mamh.gouv.qc.ca/documentsfinanciersweb/Rapport-financier-2024-et-autres-45

In summary

OMHS = unavoidable future costs that the municipality will have to pay to close, dismantle, or restore its public infrastructure.

Failing to plan for these costs now may end up costing citizens more later on.

Conclusion

Yes, my tone may seem harsh toward the administration; nevertheless, this point had to be raised in discussions about municipal debt. The municipality must now identify and evaluate its OMHS. I didn’t see anything in the PowerPoint presentation from September 16. Should we be concerned?

The financial auditor requires this to avoid a new audit reservation. This means incorporating these obligations into the budget preparation process and clearly communicating the fiscal impacts on the 2023, 2024, 2025, and future budgets to citizens. To my knowledge, no details on OMHS have been presented at this time.

I hope this has helped you learn a little more. For my part, I found the exercise very constructive!