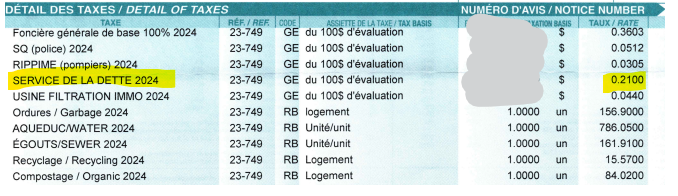

In my view, the village’s debt is a priority: it incurs significant financing costs ($346,440 in 2024). Each taxpayer contributes, through their municipal taxes, a portion dedicated to repaying this debt: $0.21 per $100 of assessed value. This represents $1,205.40 for a house valued at $574,000 (average property value in North Hatley in 2025).

Reference: 2024 residential tax account in North Hatley with the amount paid to repay the debt.

It must therefore be reduced in order to move forward. You know that several citizens questioned this following the September 6 newsletter, and Mr. Reed was served with a formal notice by a bailiff following his questions about public finances, which you can read here.

Please excuse me: it is precisely this reaction from the municipality that prompts me to delve deeper into the subject.

Definition of financing costs (According to ChatGPT)

Financing costs: a broader category that sometimes includes penalties/break fees, commitment fees, or interest related to leases.

- interest on debt;

- bank charges (e.g., card fees, cash advances, overdraft fees);

- issuance and borrowing costs (fees, discounts/premiums on bonds, amortized over time);

The factual observation

Since 2023 and again in 2024, the independent auditor has issued a qualified opinion on North Hatley’s financial reports. The basis for this opinion is the same from one year to the next: the municipality has not assessed or recorded certain liabilities related to the decommissioning of capital assets (OMHS), nor has it provided the required information, which constitutes a departure from public sector standards. The auditor specifies that the impact could not be quantified.

It is important to note that since April 2022, public sector accounting standard PS 3280 requires all municipalities in Quebec to:

✔️ identify infrastructure that will eventually need to be dismantled or closed

✔️ assess the future costs associated with their decommissioning

✔️ record them as a debt (liability) in their financial statements

✔️ explain these obligations in the financial notes

This is an obligation—not a choice. Municipalities must calculate OMHS according to SP 3280, otherwise they will receive a qualified opinion from the auditor. This includes financial reports issued with a qualified opinion.

In concrete terms, what this changes

- Budget predictability: risk of “unpleasant surprises” (late adjustments).

- Taxes and rates: potential pressure on tax bills or water/waste rates.

- Investment priorities: projects may be postponed to finance these obligations.

- Borrowing capacity: unrecognized future expenses may complicate financing.

- Transparency: public trust depends on complete and compliant financial statements.

Specific (constructive) questions to ask in public session

- Correction schedule: When will the OMHS assessment be completed and incorporated into the statements?

- Methodology: What method (estimation, assumptions, discount rate) will be used to calculate the OMHS?

- Potential scale: within a conservative range, what order of magnitude could be expected (low/medium/high scenarios)?

- Budgetary impact: What would be the repercussions on net debt and budgetary choices (taxes, investments, maintenance) if OMHS were recognized?

- Governance: what responsibilities (management/partnerships) and what monitoring (committee, deadlines) are needed to ensure that the reserve is not repeated in 2025?

| Year | Audit opinion | Conclusion |

| 2021 | Clean opinion | Compliant |

| 2022 | Clean opinion | Compliant |

| 2023 | Qualified opinion | Accounting anomaly |

| 2024 | Qualified opinion | Accounting anomaly Uncorrected situation |

Reference: Analysis of financial reports audited by auditors

What reserve means (according to ChatGPT)

- Overall reliable: apart from this point, the auditor considers that the financial statements give a true and fair view.

- Blind spot: the lack of assessment/accounting for OMHS creates a shortfall in future obligations (e.g., closure/restoration of infrastructure) that could affect net debt in the long term.

Conclusion

Based on my understanding of best practices in municipal finance, it is essential to assess, disclose, and plan for OMHS in our financial statements to avoid unpleasant surprises.

Based on my reading of the municipality’s 2021-2025 financial presentation PowerPoint, there is no mention of this.